Grocery Stores With 9% Dividend Yield Trading At A 30% Discount: Too Good To Be True?

Important Note

Some of our best investments in recent years have been retail REITs.

Retail used to be hated due to the false notion that e-commerce was killing retail properties and this allowed us to accumulate large positions at discounted prices in a number of mall and strip center REITs from 2018-2021.

But more recently, the market has realized that it had overreacted, and as a result, the share prices of these retail REITs have surged to new highs.

Retail has now become one of the hottest property sectors because the lack of new supply is leading to rapid rent growth.

This has pushed us to do a lot of research on various retail REITs, hoping to find new opportunities to present to you, and that's how I recently came across Slate Grocery REIT (SGR.U:CA; SRRTF).

At first, I thought that this had the potential to be our next big winner. The REIT owns very desirable properties with rents that are below market, and yet, its stock is still heavily discounted relative to its peers.

However, after digging deeper, we uncovered issues related to its financial management and conflicts of interest, which make it far less desirable.

Sometimes, I feel pressured to present new opportunities at High Yield Landlord to keep it more exciting, but the reality is that there are times when new opportunities are rare, and we are better off just sticking to what we already own.

This is the case here, and this is why we have decided not to invest in the company. Since many of you have asked about it on our chat, we are still sharing our research below.

We think that the best opportunity in this sector remains RioCan (REI.UN:CA) and you can read about it by clicking here. Note that we will also share another better opportunity later this week so stay tuned for that.

Slate Grocery REIT: Good Assets And Bad Financial Management

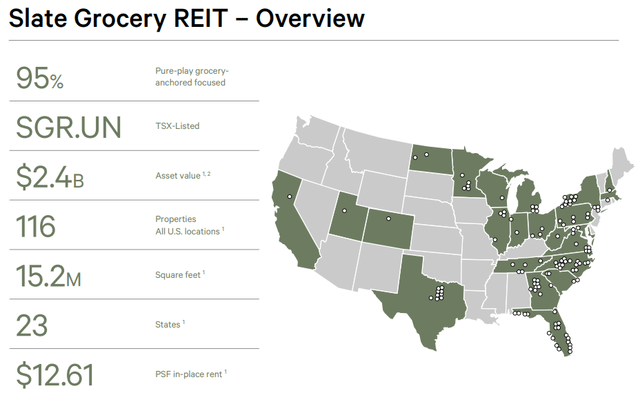

Slate Grocery REIT is a unique and little-known REIT. It trades on the Toronto Stock Exchange and only over-the-counter in the US, but 100% of its properties are located in the US, making it akin to BSR REIT (BSRTF).

Slate is a grocery-anchored shopping center REIT with highly defensive qualities, and yet it trades at about a 30% discount to NAV. Why?

We believe there are three primary reasons that Slate Grocery REIT has underperformed and been valued so cheaply by the market:

The REIT is externally managed by Slate Asset Management, the same manager that overleveraged Slate Office REIT (SLTTF, SOT.UN:CA) and destroyed virtually all shareholder value during its decade-long existence as a public REIT. Also, the management fee for Slate Grocery increases based on gross book value, and the external manager is paid fees for acquisitions. Obviously, these two incentives would seem to motivate management to grow the portfolio without necessarily growing AFFO per share.

Debt is fairly high at 52% of GBV (asset value based on acquisition costs). Much of this debt only recently became fixed-rate, which has caused Slate's interest expenses to increase meaningfully.

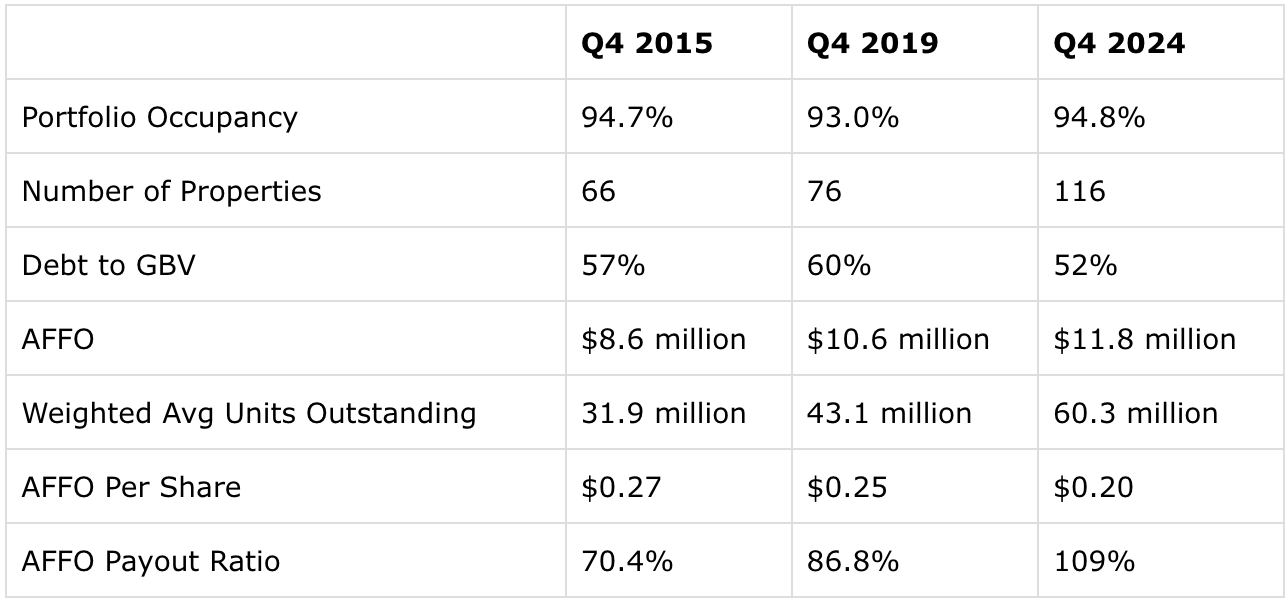

AFFO per share has gradually declined over time while the dividend has stayed basically flat, resulting in a rising payout ratio. As of Q4 2024, the AFFO payout ratio reached 109% (!!).

That said, Slate Grocery also has a number of positives going for it that Slate Office REIT never did:

Grocery-anchored shopping centers have become more in demand among both tenants and investors in recent years, in part because grocery has proven itself to be resistant to disruption from e-commerce.

Occupancy is strong at 94.8%.

98% of tenants are on net leases, which reduces operating expenses and increases the stability of cash flows.

In-place rents are below-market, even with operating expense reimbursements taken into account.

About 95% of debt is effectively fixed-rate.

The external manager owns 5.6% of common stock, increasing alignment with shareholders.

How do we put together this assortment of pros and cons? Is Slate Grocery a deep value or a value trap?

The REIT offers an astounding 8.8% dividend yield, paid monthly, but there is of course a reason for Slate Grocery's cheap valuation and high yield.

Its closest peers, Phillips Edison & Company (PECO) and InvenTrust Properties (IVT), both grocery-anchored retail REITs, trade at dividend yields of around 3%.

In what follows, we discuss why Slate Grocery's assets are appealing even though its financial management is very unappealing.

We recommend that REIT investors steer clear of this name.

The Appeal of Grocery-Anchored Shopping Centers

First, let's explore why grocery-anchored retail real estate is appealing.

In short, essential retail such as shopping centers anchored by a grocery store or superstore like Walmart (WMT) or Target (TGT) is both recession-resistant and resilient to e-commerce. Better yet, in today's world, both physically native and digitally native retailers increasingly want to hone omnichannel strategies that include both physical stores and robust online platforms.

While retail generally does well in both economic expansions and mild to moderate recessions (such as the early 2000s slump), grocery retailers are particularly resilient in good times and bad.

Grocers tend not to grow sales as fast as non-grocery retailers during expansions, but their sales growth slows less than non-grocery retailers during recessions.

Since grocers make up such a substantial portion of total rent from a grocery-anchored shopping center (typically 30-60%), the total rental income from these properties tend to be more stable than for non-grocery-anchored retail properties.

Although consumer spending at restaurants & bars has grown far faster than at grocery stores in the post-COVID era, this is not as disappointing for grocery-anchored centers as it may seem, as grocery-anchored centers also sometimes feature restaurants and bars within their main building or in outparcels in the parking lot.

What's more, given soaring credit card debt in the US, the balance of spending may shift back toward grocery stores soon.

But whether retail spending is in essential goods or discretionary goods, steadily rising retail sales is definitely supportive of retail real estate and enables retailers to pay higher rents over time.

Notice also the darker line in the chart above, which shows that retail square footage per capita has been slightly but steadily falling over the last 15 years.

That is because, as the left-hand chart below shows, there has been very little new supply of strip centers delivered to market in the last 15 years.

Notice in that left-hand chart that, aside from brief periods in 2011, 2017, and 2020, net absorption of retail space in strip centers has been meaningfully higher than new supply being delivered. The natural result of this has been falling vacancy rates and rising rents, as you can see on the right-hand chart.

Grocery-anchored shopping centers may not be the sexiest area of commercial real estate, but they do offer extremely stable and reliable growth in cash flows over time.

Slate Grocery REIT: Asset Stability And Defensive Growth

Now, turning to Slate Grocery's portfolio, we find a lot to like.

First off, the portfolio is 95% grocery-anchored shopping centers, higher than any other publicly traded REIT. PECO is the only similar REIT with such high exposure to grocery stores in the US:

On top of this, about 70% of Slate's gross leasable area is occupied by what the REIT considers "essential retail" tenants.

As you can see above, the vast majority of Slate's portfolio is located in the Eastern half of the United States. About 60% of Slate's portfolio is concentrated in Sunbelt states, with Florida accounting for the largest share of GLA at 16% and Dallas the single largest market at 6%.

While being in the Sunbelt is an advantage in the sense that the population is growing while supply growth is limited, Slate is also located in other parts of the country with dense populations and high barriers to entry for new supply. Examples of these types of areas are New York and California.

Here's how the portfolio's tenancy breaks down:

Almost half of Slate's gross leasable area consists of grocery stores and supermarkets, while another 9% are other necessity-based retailers.

One of the most interesting aspects of Slate is that, like Whitestone REIT (WSR), the vast majority of its leases are net leases, meaning that the tenants are financially responsible for all or most taxes, insurance, and maintenance (including for common areas).

Of course, rent rates are lower (averaging $12.41 per square foot compared to $20-22 PSF for strip centers with gross leases) with net leases, but Slate's operating expenses are also significantly lower.

How this works in practice is that Slate pays common area maintenance, property taxes, and insurance, and then bills these expenses out to tenants for reimbursement.

Slate also generates revenue from percentage rent (often paid by regional and mid-sized grocers) as well as ground rent on outparcels and other minor forms of revenue.

These reimbursements on operating expenses really smooth out Slate's financial performance over time.

As you can see from the image above, this net lease model provides high stability of cash flows while also generating inflation-beating revenue growth from lease-over-lease rent increases.

Net leases usually have multiple option periods of 1-5 years each at the end of their initial terms, and these option periods typically come with predetermined rent escalations. But when all option periods expire, the landlord and tenant negotiate new rent, which typically jumps up closer to the market rent rate, if contractual rent increases have been slower than market rent growth.

That's exactly what we see with Slate. The REIT reported lease renewal spreads for non-option tenant renewals of ~13% for the full year of 2023. Including option periods, Slate's spreads on total leasing in 2023 was slightly over 10%.

That is remarkable organic growth for a sleepy, essential retail REIT!

Balance Sheet: Debt-Heavy With Some Near-Term Maturities

When it comes to the balance sheet, we begin to see Slate's vulnerability.

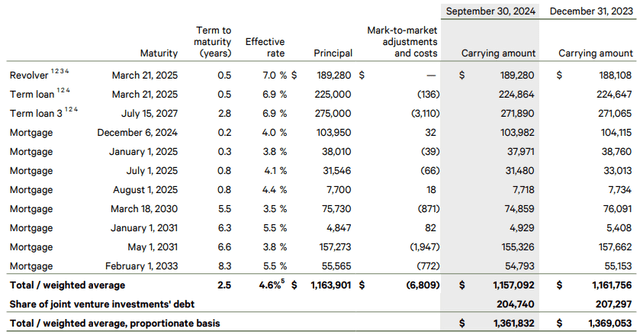

Historically, Slate's debt to gross asset value (based on acquisition price) has been between 50-60%. Currently, it is on the low end at 52%.

Including the interest rate swaps in place on its floating rate term loans, about 95% of Slate's debt is effectively fixed.

As you can see above, Slate has some relatively low interest rate mortgages maturing this year and it will almost certainly have to refinance at meaningfully higher interest rates.

This will pressure Slate's dividend coverage even further and likely force it to cut it.

Key Metrics Over Time

It's useful to look at Slate's key performance metrics over time.

Going back to the final quarter of 2015, we find that Slate's portfolio occupancy has been basically flat even while its portfolio has nearly doubled and debt to gross book value ("GBV") has fluctuated between 50% and 60%.

How has the portfolio grown so much while keeping leverage ratios within the same band? The answer is huge equity issuance, as you can see from the growth in weighted average units outstanding.

Now, if Slate had a strong (read: low) cost of equity, then this equity issuance for portfolio growth wouldn't be a problem. But Slate has never had a low cost of equity. At its highest price in 2021, the REIT's AFFO yield still stood at around 8% -- well above the 6-7% cap rates for grocery-anchored shopping centers.

The formula has been to offset high-cost equity with relatively lower-cost debt. (Of course, that formula only works when interest rates are adequately low.)

Hence the fact that AFFO per share has drifted lower and the payout ratio risen higher over time.

The reasoning for the rising payout ratio given by management on the Q4 2023 conference call was that leasing volume has been high lately and leasing/tenant improvement costs are eating into AFFO.

But leasing and TI costs are just a short-term cause for the rising payout ratio. The long-term cause has been dilutive equity issuance.

Valuation

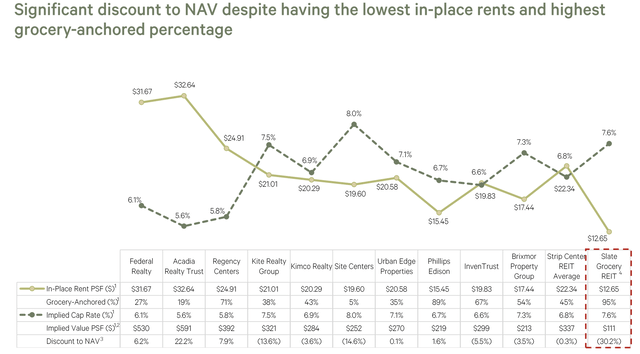

Slate Grocery REIT highlights the fact that their stock is valued very cheaply even while their in-place rents per square foot are very low.

Of course, most of Slate's peers listed above use modified gross leases, where tenants pay a higher rent plus their own utilities (and sometimes their pro-rata share of common area maintenance) but the landlord pays for other operating expenses like taxes and insurance.

If we included reimbursed operating expenses into Slate's rent PSF, the REIT's in-place rent PSF would jump to ~$16.50.

However, even with this adjustment, we can see that Slate's in-place rents are still below peers'.

PECO would be Slate's closest peer because of its focus on grocery-anchored centers and similar use of net leases. PECO's in-place rent PSF, including reimbursements, would be over $19.00 -- 15-20% higher than that of Slate.

So, Slate's presentation of their portfolio's in-place rents being below-market seems to be accurate, but it could also just tell us that their own lower quality properties.

We think that the discount to NAV and low implied value PSF have to be seen in light of the REIT's poor track record when it comes to financial management.

Bottom Line

Although Slate Grocery REIT's essential retail properties are attractive, we cannot recommend this REIT.

The dividend looks unsafe, and if management cut it, we believe that would cause a selloff in the stock price, thus reinforcing its low valuation and high cost of equity.

We would be happy to own these grocery-anchored retail properties if a different management team with more shareholder-aligned incentives was in place, but sadly, that is not the case. Finally, please note that we exceptionally posted this article without a paywall. If you found it valuable, consider joining High Yield Landlord for a 2-week free trial.

You will also gain immediate access to my entire REIT portfolio, real-time trade alerts, exclusive REIT CEO interviews, and much more. We are the largest and highest-rated REIT investment newsletter online, with over 2,000 paid members and more than 500 five-star reviews.

We spend thousands of hours and over $100,000 per year researching the market for the most profitable investment opportunities, and we share the results with you at a tiny fraction of the cost.

Get started today - the first 2 weeks are on us:

Analyst's Disclosure: I/we have a beneficial long position in the shares of all companies held in the CORE PORTFOLIO, RETIREMENT PORTFOLIO, and INTERNATIONAL PORTFOLIO either through stock ownership, options, or other derivatives. High Yield Landlord® ('HYL') is managed by Leonberg Research, a subsidiary of Leonberg Capital. All rights are reserved. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. The newsletter is impersonal and subscribers/readers should not make any investment decision without conducting their own due diligence, and consulting their financial advisor about their specific situation. The information is obtained from sources believed to be reliable, but its accuracy cannot be guaranteed. The opinions expressed are those of the publisher and are subject to change without notice. We are a team of five analysts, each contributing distinct perspectives. Nonetheless, Jussi Askola, the leader of the service, is responsible for making the final investment decisions and overseeing the portfolio. We do not always agree with each other and an investment by Jussi should not be taken as an endorsement by other authors. Past performance is no guarantee of future results. Our portfolio performance data is provided by Interactive Brokers and believed to be accurate but its accuracy has not been audited and cannot be guaranteed. Our portfolio may not be perfectly comparable to the relevant index. It is more concentrated and may at times use margin and/or invest in companies that are not typically included in REIT indexes. Finally, High Yield Landlord is not a licensed securities dealer, broker, US investment adviser, or investment bank. We simply share research on the REIT sector.